Key takeaways

- Scope 3 is not just a reporting topic – it increasingly functions as a decision-making lens for core business choices.

- A fragmented Scope 3 approach leads to management frustration, supplier disengagement and delays in tenders, audits and client decisions.

- Client expectations, data depth and scrutiny are increasing year on year – postponing structure today often creates reactive pressure tomorrow.

- A structured Scope 3 approach improves supply chain resilience, supports product and investment decisions, and strengthens commercial credibility.

- CSRD acts as a stress test for the value chain, exposing where data, assumptions and supplier relationships are not yet robust.

Scope 3 CO₂ emission reduction: what can your company realistically achieve?

Chances are that your Scope 3 CO₂ emissions represent the largest share of your total carbon footprint, as is the case for most organisations. They are also the most complex to manage, since they are largely outside your direct operational control.

This creates a strategic dilemma: you are held accountable for the emissions throughout your entire value chain – including Scope 3 emissions – through client expectations, investor scrutiny and regulations such as the Corporate Sustainability Reporting Directive (CSRD), while the underlying activities often sit outside of your control, with suppliers, customers or partners.

As a result, you might find yourself investing significant time and resources into Scope 3 data collection, only to end up with fragmented data, limited confidence in the results and little strategic steering power. Your team could spend months chasing suppliers, and the output could be difficult to interpret. In that sense, CSRD does not introduce new issues as much as it functions as a stress test for the value chain – revealing where data, relationships and assumptions no longer hold up under scrutiny.

So, what is a smart way to tackle this? The key to answering this question is a shift in perspective: it’s not about whether you can control Scope 3 emissions, but how you can meaningfully influence them.

Those organisations that make progress do not attempt to “own” their entire value chain. Instead, they focus on governance, procurement, supplier engagement and product lifecycle decisions. Approached this way, Scope 3 shifts from a recurring reporting headache to a framework that supports clearer investment priorities, more credible client conversations and less ad hoc pressure late in the reporting cycle.

This article explores where that influence realistically lies, what credible action looks like, and how your organisation can move from perceived dependency to deliberate value-chain leadership.

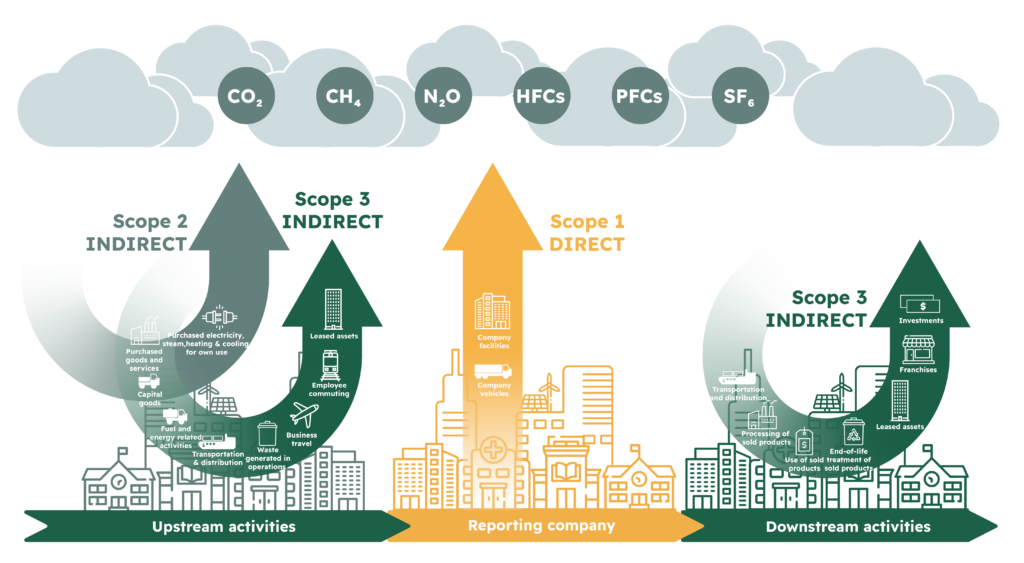

What are Scope 3 emissions?

Scope 3 emissions are all indirect greenhouse gas emissions that occur in your company’s value chain, excluding Scope 2 purchased energy. The definition follows the Greenhouse Gas Protocol and covers both upstream and downstream activities, including:

- Purchased goods and services

- Capital goods

- Upstream and downstream transport and distribution

- Use of sold products

- End-of-life treatment of products

Unlike Scope 1 and 2 emissions, Scope 3 emissions do not come from your company’s own buildings, vehicles or equipment. They occur elsewhere in the value chain, for example at suppliers or during the use of products.

Even though you do not directly control these emissions, they often influence how your organisation is evaluated – in tenders, audits, financing decisions and sustainability assessments. In that sense, Scope 3 emissions can affect commercial opportunities, cost exposure and reputation, even when they sit outside your operational boundaries.

Why this matters strategically

Scope 3 goes far beyond carbon accounting or sustainability reporting.

Handled well, it becomes a decision-making framework for core business choices. Scope 3 increasingly shows up at moments where decisions need to be made: approving investment plans, responding to tenders, signing long-term contracts or defending sustainability claims. When insight is incomplete or inconsistent, decisions could be delayed – or taken with uncertainty. In other words, a weak or fragmented Scope 3 approach becomes a bottleneck, resulting in:

- sustainability transition plans that are questioned or rejected

- lower EcoVadis scores due to inconsistent data and documentation

- delays in deals or tender processes while data is clarified

- reputational exposure when claims cannot be substantiated

If you do not take a structured approach to Scope 3, you are, in effect, making strategic decisions without a full view of your exposure and dependencies.

In practice, Scope 3 insights directly inform:

- Supply chain resilience

Understanding where emissions sit often reveals where dependencies, bottlenecks or concentration risks exist. This supports more informed sourcing decisions and reduces vulnerability to disruption, price volatility or regulatory change. - Product and service strategy

Scope 3 hotspots frequently align with the most carbon- and cost-intensive parts of a product’s life cycle. That insight could help you prioritise redesign, alternative materials, circular models or service-based offerings that strengthen your competitiveness over time. - CAPEX and OPEX choices

Decisions on equipment, infrastructure, outsourcing or logistics increasingly have long-term emissions and cost implications. Scope 3 provides a lens to assess trade-offs between upfront investment, operational cost and future risk. - Client trust and commercial credibility

Clients are no longer satisfied with generic commitments. They expect suppliers to understand their footprint, explain priorities and demonstrate progress. A structured Scope 3 approach enables credible, consistent answers – and avoids reactive ‘firefighting’. - Board-level accountability and governance

Scope 3 translates sustainability into strategic risk and opportunity, making it discussable at board level in terms of resilience, growth and long-term value – not just compliance.

If you finetune your Scope 3 approach today you are better prepared for the conversations ahead – not only with regulators, but with boards, procurement teams and key clients.

Ultimately, how your organisation handles Scope 3 increasingly influences its position in the market – not only how it reports, but how credible, reliable and future-ready it is perceived to be by clients and partners.

Influence instead of ownership

Scope 3 emission reduction does not require full control, but deliberate influence. Organisations that make progress do so not by managing every operational detail in the value chain, but by using their position strategically.

Influence emerges where choices, expectations and collaboration intersect. Below are four concrete actions you can take that move the needle:

1. Use procurement as a strategic lever

Procurement policies are more than compliance documents. They are direction-setting instruments.

By embedding sustainability into:

- supplier selection

- contractual requirements

- evaluation and tender criteria

your organisation sends a clear signal: ‘sustainability is integral to how we do business’. Even without direct control over suppliers, awareness across the value chain begin to shift.

2. Make expectations explicit – and engage suppliers beyond questionnaires

Not all organisations have clear sustainability expectations towards their suppliers. In practice, data requests are often triggered by external pressure: client questions, reporting requirements or data gaps that surface late in the reporting cycle. When these requests feel ad hoc or repetitive, suppliers disengage, response rates drop and data quality suffers.

Making expectations explicit early on – while being transparent about where your own approach is still evolving – helps shift the conversation. Instead of reactive data chasing, organisations create clearer alignment on priorities, feasibility and credibility.

Organisations that move ahead combine this clarity with active supplier engagement, for example through:

- explaining why data is needed and how it will be used

- aligning assumptions and methodologies

- investing in shared learning, such as workshops on sustainability and carbon accounting

In practice, this leads to:

- improved data quality

- greater willingness to collaborate

- fewer frictions during reporting, audits and client questionnaires

- less internal time spent reconciling inconsistent datasets

The result is not only better Scope 3 insight, but a more stable and scalable way of working with suppliers over time.

3. Extend your product lifecycle

For some business models, a significant share of Scope 3 emissions does not sit in procurement, but in use and end-of-life.

Exploring options such as:

- refurbishment

- reuse

- service and maintenance models

can significantly reduce overall impact while creating additional value.

A concrete example is Idé Coffee, who extend the life of their coffee machines through refurbishment. This reduces the need for new production, lowers Scope 3 emissions, and strengthens a circular value proposition towards clients.

What to do when reduction reaches its limits

Not all emissions can be avoided today. Handling the remainder with integrity matters.

Carefully considered compensation, embedded in a broader reduction strategy and communicated transparently, can play a role here. Not as a shortcut, but as a final step once meaningful reduction efforts have been pursued.

Frequently asked questions about Scope 3 emissions

Can companies really influence Scope 3 emissions?

Yes. While companies do not directly control Scope 3 emissions, they can exert meaningful influence through procurement policies, supplier engagement, contract requirements, product design choices and collaboration across the value chain.

What are credible Scope 3 reduction actions?

Credible actions include integrating sustainability into procurement decisions, engaging suppliers on data and reduction pathways, extending product lifecycles through reuse or refurbishment, and prioritising high-impact value-chain hotspots rather than attempting blanket control.

Is Scope 3 reporting mandatory under CSRD?

Yes. CSRD requires companies to report Scope 3 emissions as part of their climate disclosures, aligned with recognised methodologies such as the Greenhouse Gas Protocol.

My company is not directly subject to the CSRD. Should I still care about Scope 3 emissions?

Yes. Even if your organisation is not directly subject to CSRD, you could be indirectly affected through your role in other companies’ value chains. Larger clients that are in scope of CSRD must report on their Scope 3 emissions, which include emissions from suppliers – so they might request emissions data from you.

When is carbon compensation appropriate for Scope 3?

Compensation can be considered once reduction options have been meaningfully explored. It should be used transparently, as a complement to – not a substitute for – reduction efforts, and embedded within a broader climate strategy.

Our role at The Ecological Entrepreneur

At The Ecological Entrepreneur, we support organisations across their full sustainability journey, always tailored to context and maturity:

- from CO₂ baselines to reduction strategies

- from materiality assessments to value chain engagement

- from reporting and target setting to credible compensation

Sounds like a fit?