In January 2025, the CSRD officially came into effect, creating a massive shift in the corporate reporting landscape. Companies are required to share insight into their sustainability data and how they are addressing sustainability issues. The directive assumes a broad approach to sustainability, taking into account not just the environmental impact of entrepreneurship, but looking at the social and governance aspect as well, and that for the entire value chain. The legislation will be introduced in phases, starting with the largest companies first (estimated to be 40% of EU companies).

What is the CSRD?

The CSRD, the Corporate Sustainability Reporting Directive, aims to standardise and enhance sustainability reporting requirements for companies operating in the EU. Specifically, this means that companies are required to disclose transparent and detailed information on environmental, social, and governance (ESG) matters.

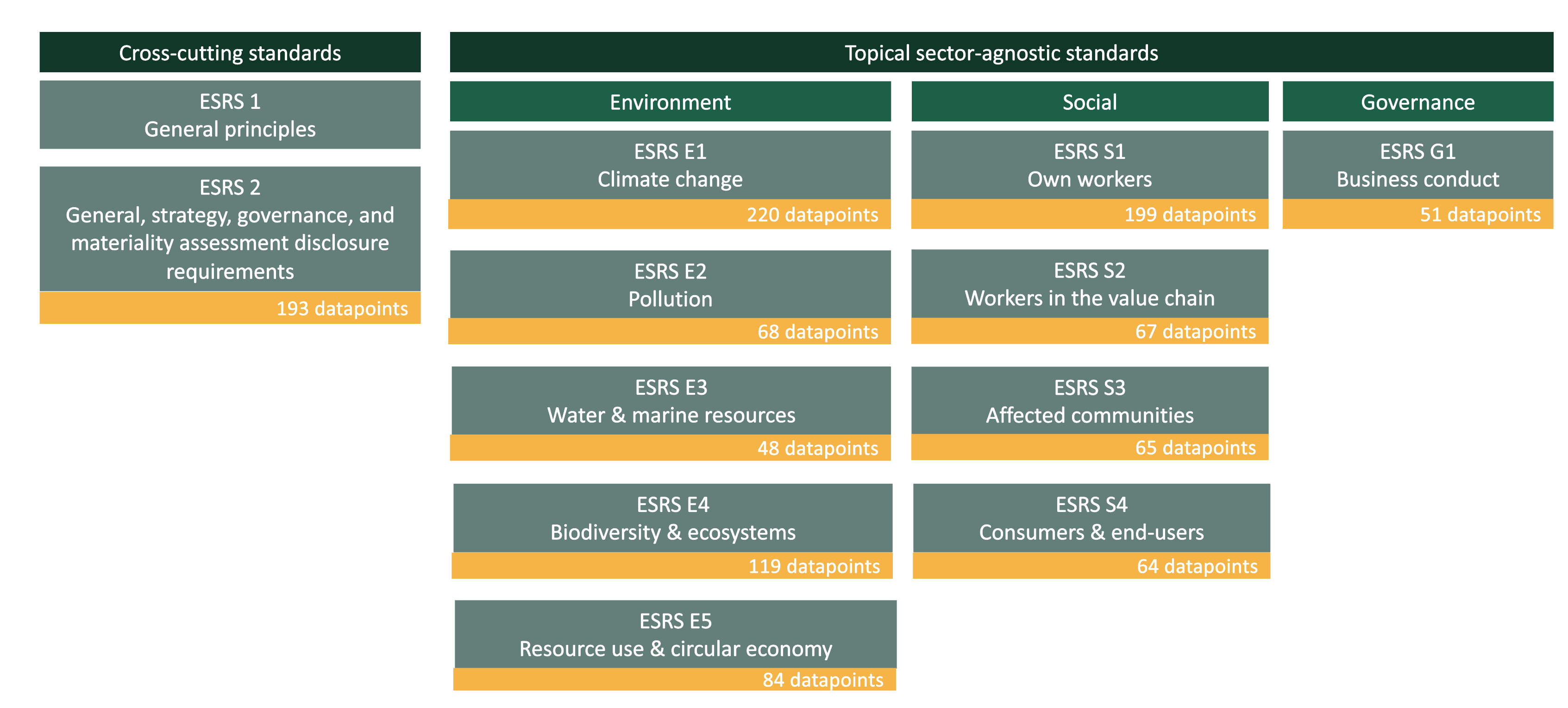

The CSRD lists 1144 data points to report on, over 10 ESG-related themes. The directive is translated into the ESRS, the European Sustainability Reporting Standards.

The CSRD implementation timeline

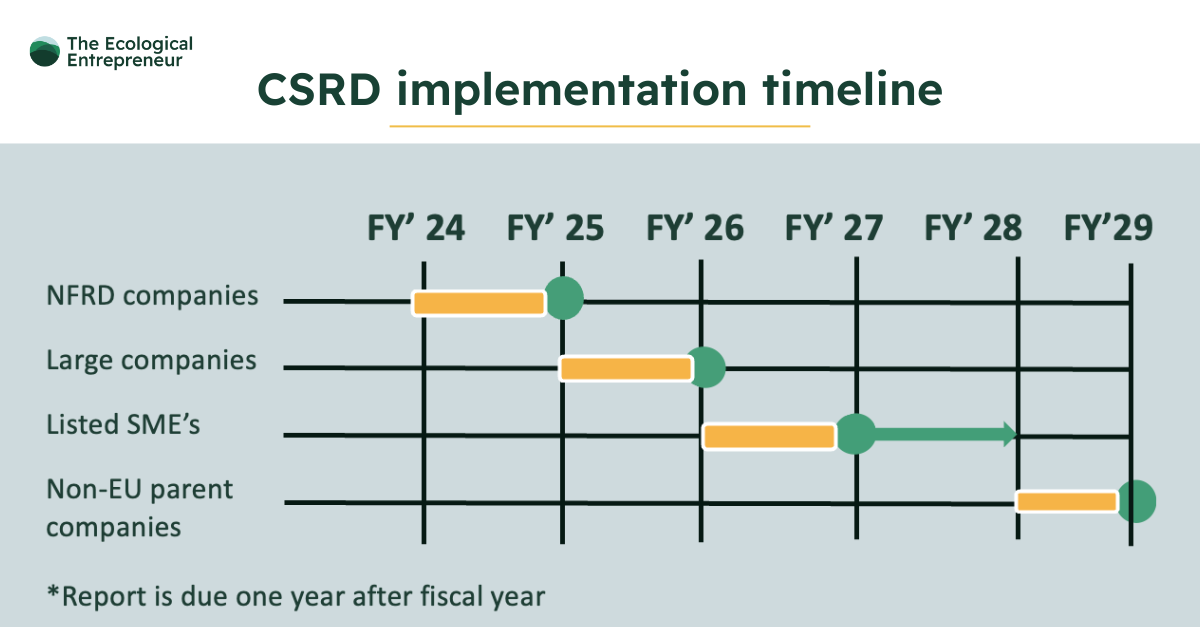

The CSRD will be rolled out in four phases, starting with the largest companies first:

1: NFRD companies

For NFRD companies, the first report is due in 2025, reporting on the fiscal year 2024. These companies are defined by more than 500 employees and a turnover of over 40 million euro.

NFRD stands for Non-Financial Reporting Directive. This 2014 directive is in some ways a precursor of the CSRD. It compelled affected companies to disclose non-financial information in their annual reports. These ‘NFRD companies’ will now be the first to be targeted by the CSRD.

2: Large companies

Large companies will be expected to submit their first report in 2026, reporting on 2025. These companies are defined by 2 out of 3 of the following criteria:

- + 250 employees

- + 50-million-euro turnover

- + 25 million in assets

3: Listed SMEs

For listed SMEs, the first report is due in 2027, reporting on 2026. This category consists of all listed SMEs in Europe, except micro-undertakings. An extension until 2028 is possible, if the company can provide substantiated reasons for this.

4: Non-EU companies

In 2029, non-EU parent companies with a large activity in the EU are expected to report on 2028. These are companies with a turnover of over 150 million euro and at least one subsidiary or branch in the EU.

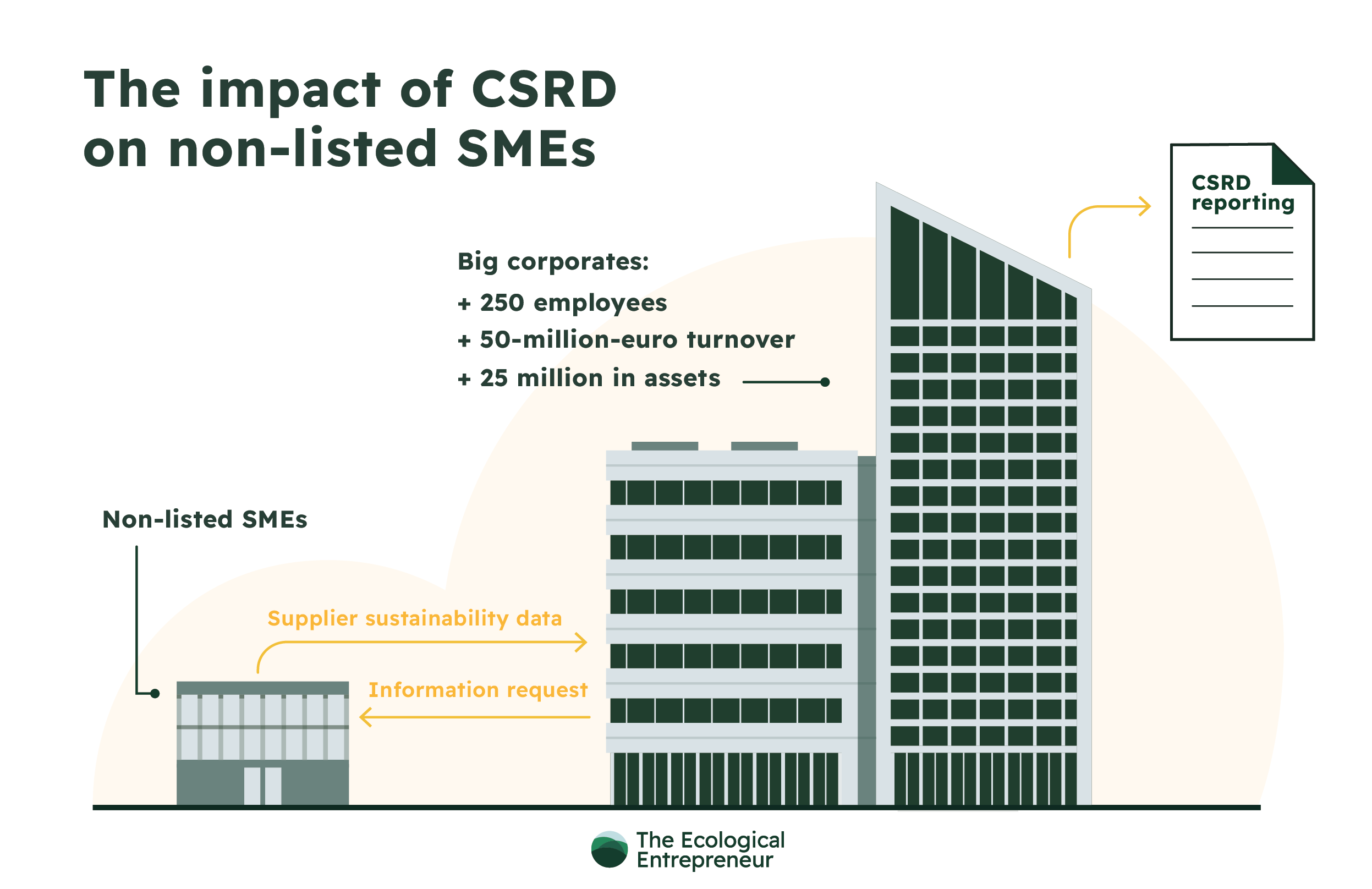

What if your company falls outside the direct scope of the CSRD?

If your organisation does not fall into any of the above-mentioned categories, don’t rejoice just yet. Non-listed small-to-medium companies are often still affected by the CSRD indirectly. If you supply to a larger company that does fall directly under the directive, your client will expect you as their supplier to provide them with the necessary sustainability data. Because adequate CSRD-compliant reporting requires them to acquire information on the entire value chain, including, for example, their suppliers’ data on carbon emissions. And considering the learning curve involved when first conducting a CO₂-analysis, you would be wise to start taking action today, if you haven’t already.

To provide a digestible framework for companies that fall outside the direct scope of the CSRD, but might still be affected indirectly, EFRAG (the European Financial Reporting Advisory Group) developed the Voluntary Sustainability Reporting Standards for SMEs (VSME). These can serve as guidelines for sustainability reporting for non-listed SMEs. They are less comprehensive than the ESRS, but still in line with the CSRD disclosure requirements. In this way, as a non-listed SME, you can respond to the questions you will receive from partners, customers, suppliers, and other key stakeholders.

Need more information?

If you want to expand your understanding of sustainability legislation and prepare for the impact of the CSRD, check out our online course on the topic:

Are you specifically interested in the CSRD’s impact on SME’s? Check out our blog post on this particular topic.

Or, if you prefer a more personal approach, reach out to us!